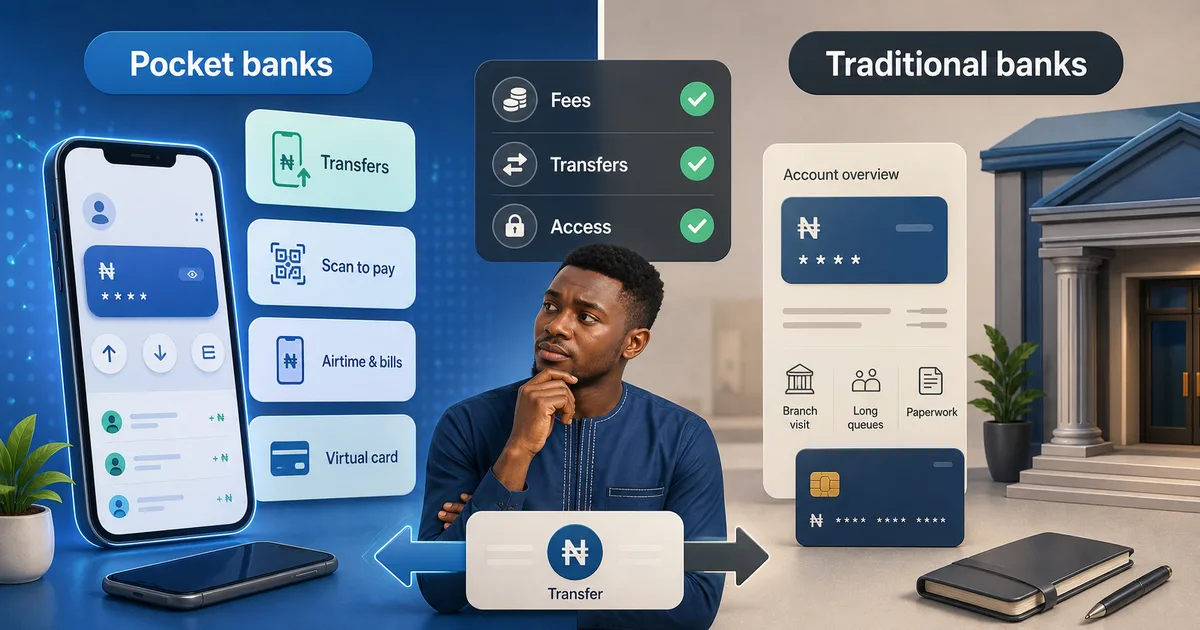

Nigeria has two banking systems now. On one side are the traditional banks you grew up with: GTBank, Access Bank, UBA, First Bank, and Zenith. On the other side are pocket banks (fintech banks) like OPay, PalmPay, Kuda, and Moniepoint. These newer platforms have grown fast, especially among younger Nigerians who want banking on their phones without paperwork and queues. But are they truly better? This comparison covers fees, transfers, loans, customer service, reliability, and more. By the end you will see why most Nigerians are better off using both.

What Are Pocket Banks in Nigeria?

Pocket banks are financial apps offered by fintech companies. They let you open a bank account from your phone in minutes with no paperwork. In Nigeria the biggest players are OPay, PalmPay, Kuda, Moniepoint, and VFD. These platforms partner with licensed banks to offer banking services. Your money sits with a partner bank underneath, but the experience is app-first, fast, and mostly fee-free.

- Most popular pocket banks in Nigeria

- OPay: Owned by Opera. Known for transfers, airtime, and bill payments. Very popular for everyday transactions.

- PalmPay: Backed by Chinese investors. Heavy on cashback and rewards. Strong POS network across Nigeria.

- Kuda: Nigerian-founded. Marketed as the bank of the free. No maintenance fees. Built-in budgeting tools.

- Moniepoint: Dominates business payments and POS terminals. Recently expanded to personal accounts with a full banking license.

- VFD: Parent company of several fintech brands. Less consumer-facing but powers multiple financial platforms across the country.

What About Traditional Banks?

Traditional banks in Nigeria include GTBank (now Guaranty Trust Holding Company), Access Bank, First Bank of Nigeria, UBA (United Bank for Africa), and Zenith Bank. These established players have physical branches, decades of history, and full banking licenses. They offer everything from savings and current accounts to loans, foreign exchange, international wire transfers, and business banking. They are regulated by the Central Bank of Nigeria (CBN) and covered by the Nigeria Deposit Insurance Corporation (NDIC) up to ₦500,000 per depositor.

- Top traditional banks in Nigeria

- GTBank: Known for innovative digital banking and strong app experience. Popular among retail and corporate customers alike.

- Access Bank: One of the largest banks in Africa. Strong loan portfolio and international presence across multiple countries.

- First Bank: Nigeria's oldest bank. Widest branch network. Trusted for long-term banking relationships.

- UBA: Pan-African presence in 20+ countries. Strong in remittances and international money transfers.

- Zenith Bank: Industry leader in profitability. Known for corporate banking and reliable service quality.

Account Opening: Which Is Faster?

Pocket banks win this category convincingly. You download the app, take a picture of your BVN, snap your face for verification, and you are done in under five minutes. No paperwork, no queue, no reference letter. Your account is active immediately and you can start receiving money within minutes.

Traditional banks require more steps. Even with their apps, the process often involves visiting a branch, getting a reference letter from an existing customer, or waiting days for approval. GTBank digital account opening has improved, but it still cannot match the speed of OPay or Kuda. If you need an account quickly, pocket banks are the clear winner in this category.

Fees and Charges: Where Do You Pay Less?

Pocket banks typically charge zero maintenance fees. No monthly charges, no ATM card fees on virtual cards, and no hidden deductions. Transfers between accounts on the same platform are free most of the time. This makes them ideal for daily transactions and low-balance users.

Traditional banks charge more fees. Common deductions include monthly maintenance fees, ATM card renewal fees, SMS alert charges, and stamp duty fees on deposits above ₦10,000. These may seem small individually, but over a year they add up significantly.

- Common traditional bank fees you may be paying

- Monthly maintenance fee: ₦50 to ₦500 depending on account type

- ATM card renewal: ₦500 to ₦1,000 annually per card

- SMS alert charge: ₦4 per transaction (about ₦120 per month for active users)

- Stamp duty: ₦50 on deposits above ₦10,000

- COT (Commission on Turnover): up to ₦3 to ₦5 per mille on current accounts

On fees alone, pocket banks win by a large margin. If you want to keep more of your money, fintech banks are the better choice for everyday banking.

Transfer Experience: Speed and Reliability

Pocket banks shine on transfer speed. Transfers to other users on the same platform (OPay to OPay, PalmPay to PalmPay) settle quickly. Even NIBSS Instant Payments between different banks complete in seconds most of the time.

Traditional banks have improved with NIBSS instant payments. But their apps tend to go down more frequently during maintenance windows and have stricter transfer limits per transaction. On the other hand, traditional bank apps handle high-value transfers more reliably for amounts above ₦1 million where pocket banks may flag transactions for manual review.

For everyday transfers and small amounts, pocket banks are faster and more reliable. For large transfers, traditional banks have the edge.

Customer Service: Who Answers When You Call?

This is where traditional banks have a real advantage. If you have a serious dispute (a frozen account, a failed credit, or a fraudulent transaction) you can walk into a branch and speak to a manager. Face to face service still matters when significant money is at stake.

Pocket banks rely on in-app chat, email, and phone support. For simple issues this works well. But if something goes seriously wrong, you may find it harder to get a quick resolution. OPay and PalmPay have improved their support teams, but they cannot match the accountability and escalation paths of walking into a GTBank or Access Bank branch in person.

Loan Access: Where Can You Borrow?

Traditional banks offer larger loans with better interest rates. If you have a salary account with First Bank or UBA, you can access overdrafts, personal loans, and even mortgages. Loan amounts can range from ₦50,000 to several million naira depending on your income and banking relationship.

- Pocket bank loan options

- OPay: Short-term loans through Okash, typically small amounts with higher interest rates

- PalmPay: Credit options and buy now pay later for eligible users

- Kuda: Overdraft facility up to a certain limit, subject to eligibility criteria

- Moniepoint: Business loans for merchant customers based on transaction volume

For small urgent loans, pocket banks are faster. The process is automated and you can get money in minutes. For serious borrowing above ₦500,000, traditional banks are still the better option.

POS and ATM Access

Moniepoint and PalmPay dominate the POS space in Nigeria. You can find their agents on almost every street corner. This makes cash withdrawal and deposit easy without needing a traditional bank branch nearby.

Traditional banks offer free ATM withdrawals at their own branches and sometimes at other banks. But their ATMs run out of cash more often and break down frequently. On the positive side, traditional bank debit cards work at any ATM across Nigeria and internationally if enabled.

- POS vs ATM comparison at a glance

- Moniepoint POS agents: Available everywhere including remote areas. Fees range from ₦50 to ₦200 per withdrawal.

- PalmPay POS agents: Similar coverage. Often offer cashback promotions and rewards.

- Bank ATMs: Free at your own bank, ₦35 to ₦100 at other banks. Availability is inconsistent.

- Bank branches: You can withdraw larger amounts at the counter without fees.

Savings and Investment Options

Pocket banks offer goal-based savings with attractive interest rates. Kuda savings pockets, PalmPay interest on savings, and OPay savings wallet all offer better rates than traditional savings accounts. The tradeoff is that you cannot comfortably save very large amounts on these platforms.

Traditional banks offer more investment products. Fixed deposits, treasury bills, mutual funds, and dollar-denominated accounts. If you want to invest ₦1 million or more, traditional banks have the infrastructure and regulatory coverage to handle it properly.

Security and Deposit Insurance

Read Also

Both are safe, but in different ways. Traditional banks are directly insured by NDIC up to ₦500,000 per depositor. They have been around for decades and have proven systems for handling fraud and dispute resolution.

Pocket banks store your money with partner licensed banks, so your funds are indirectly covered by NDIC. But the coverage limit applies at the partner bank level, and the claims process is less straightforward than dealing with a traditional bank directly. For small balances this is rarely an issue. For large balances, traditional banks offer more direct protection.

Reliability During Banking Crises

Pocket banks tend to be more resilient during disruptions. During the 2023 naira redesign crisis, OPay and PalmPay continued processing digital transfers while queues at traditional banks stretched for blocks. Since pocket banks deal mostly in digital money, they are less affected by physical cash shortages.

Traditional banks suffer more during cash-based disruptions. Long ATM queues, branch crowding, and system overloads are common. However, they are more stable during long-term economic downturns because they have diversified revenue streams and direct CBN backing.

International Transactions

Traditional banks win this category clearly. GTBank, Access, UBA, and Zenith offer international wire transfers, domiciliary accounts (dollar, pound, and euro accounts), and international debit cards. If you receive money from abroad or need to pay for international services, you need a traditional bank.

Pocket banks are limited here. Most do not support international transfers or foreign currency accounts. Some offer virtual dollar cards for online payments, but the functionality is limited compared to a full domiciliary account at a traditional bank.

Which Is Better? The Honest Answer

After comparing across all these dimensions, here is the truth: you should use both. Pocket banks are better for daily transactions, transfers, bill payments, and keeping fees low. Traditional banks are better for loans, international transactions, large savings, and dispute resolution. Using both gives you the best of both worlds without compromise.

- When to use pocket banks

- Daily transfers and bill payments, all fee-free or low cost

- Receiving money from friends, family, and group gifts

- Quick POS withdrawals wherever agents are available

- Keeping a low-fee account for small balances and everyday spending

- When to use traditional banks

- Receiving your salary and keeping your primary savings

- Taking out loans above ₦500,000 with better interest rates

- International money transfers and foreign currency accounts

- Saving large amounts with direct NDIC insurance protection

- Accessing investment products like treasury bills and fixed deposits

Create your first Goodiebag

Create a money packet in under 2 minutes. One link. One PIN. Everybody paid.

Create a GoodiebagWhy This Matters for Sending and Receiving Money

Goodiebag sends money gifts to OPay, PalmPay, and Moniepoint accounts through the standard claim flow. No bank delays, no withdrawal hassles, no branch visits required.

This works because pocket banks link every account to a phone number. That phone number is effectively the account number. Goodiebag uses Paystack transfers to resolve the phone number and send money. There is no need to ask for a 10-digit account number. Just the phone number and the bank name will do.

If you use both a traditional bank and a pocket bank, you already have the ideal setup. Your pocket bank handles transfers for receiving gifts and making daily payments. Your traditional bank handles long-term savings, large loans, and international transactions. The two systems complement each other perfectly.

Most Nigerians do not need to choose one system forever. A pocket bank can handle speed and daily use. A traditional bank can handle larger services and longer-term needs. Use both where they make sense.

Goodiebag Editorial Team

Goodiebag product and safety team

Guides by the Goodiebag team on social cash gifting, supported payouts, sender safety, and practical digital reward use cases in Nigeria.

Start your first Goodiebag today

Fund a drop, share a link and PIN, and let your audience claim while the moment is live. No Goodiebag account needed for recipients.

Create a Goodiebag