Long before mobile banking apps, before Paystack, before BVN numbers and POS machines, Nigerians had a system for saving money together. It was called Ajo among the Yoruba, Esusu among the Igbo, and Adashe in Hausa communities. For generations, these informal group savings circles were the only way many Nigerians could build capital, buy household items, or fund ceremonies. They worked because they were built on trust, community, and shared obligation. A group of people agreed to contribute a fixed amount at regular intervals. Each cycle, one member collected the total pool. The system rotated until everyone had their turn. It was simple. It was effective. And it did not require a bank account or even literacy. Today, that same concept is being reinvented. Digital platforms are bringing Ajo and Esusu into the 21st century, solving the old problems while keeping the community spirit alive. This article explores how group savings in Nigeria are evolving, and where the future is headed.

Important note: Goodiebag is not a savings platform, cooperative, contribution collector, deposit-taking institution, investment product, crowdfunding platform, or Ajo/Esusu manager. This article discusses possible payout coordination use cases only. Groups should use appropriate regulated or legally suitable tools for savings, contribution collection, cooperative management, or investment activities.

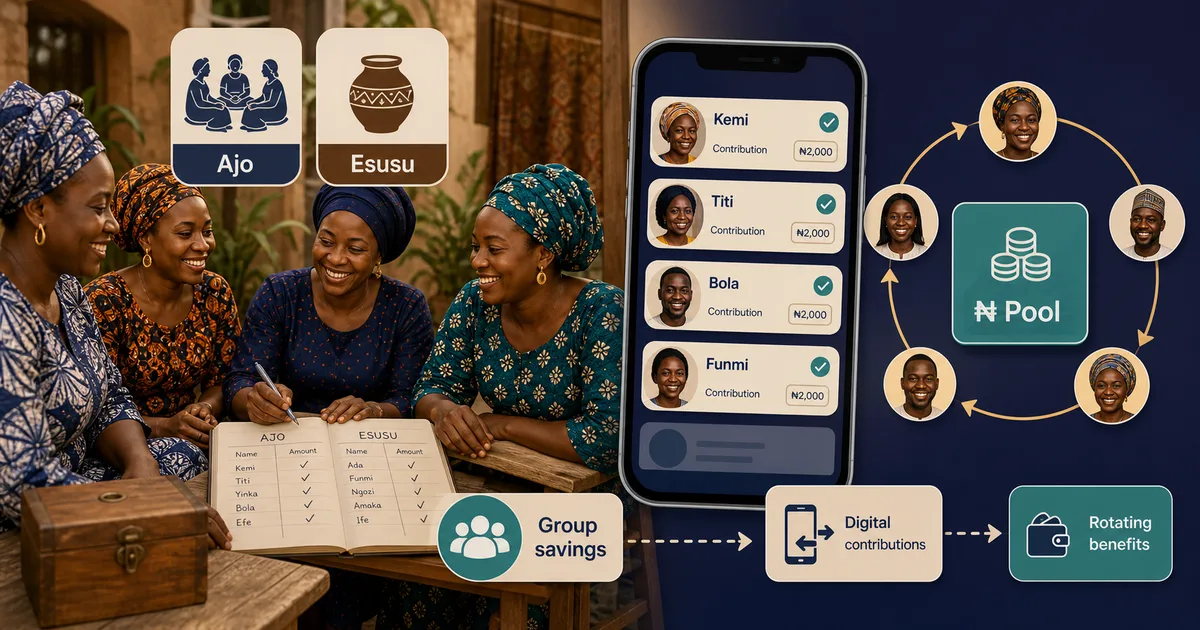

What Is Ajo and Esusu? The Cultural Origins

Ajo (Yoruba) and Esusu (Igbo) are rotating savings and credit associations. The concept is remarkably similar across Nigeria's diverse ethnic groups, with local names and minor variations but the same core mechanics. A group of people, usually between 5 and 30, agree to contribute a fixed amount of money at regular intervals, typically weekly or monthly. The total contribution is given to one member of the group on a rotating basis. If 10 people each contribute ₦5,000 weekly, the collective pool is ₦50,000. Each week, a different member receives the full ₦50,000. After 10 weeks, everyone has received their payout, and the cycle can start again.

Ajo and Esusu helped communities save before formal banking reached everyone. Market women in places like Onitsha Main Market, Balogun Market in Lagos, or Kurmi Market in Kano used contributions to restock inventory, pay children's school fees, or fund building projects. The system required no paperwork, no collateral, and no interest. It worked because members knew each other. If you failed to pay, your reputation suffered in public. That social pressure was the system's strength, but also its weakness.

How Traditional Ajo/Esusu Worked (And Still Works)

- 1Formation: A group of trusted individuals (family members, market colleagues, church or mosque members) agree to start a savings circle. A collector is chosen, often the most trustworthy person in the group.

- 2Agreement: Members decide the contribution amount (anything from ₦500 to ₦100,000 per cycle), the frequency (daily, weekly, or monthly), and the payout order.

- 3Collection: On each cycle day, members pay their contribution to the collector. Some collectors go door to door. Others designate a meeting spot.

- 4Payout: The designated recipient for that cycle receives the total pool. In some circles, the order is decided by lottery. In others, members negotiate based on urgency of need.

- 5Cycle completion: Once every member has received their payout, the group can disband, start a new cycle, or adjust the terms.

This system remains widespread across Nigeria today. EFInA's Access to Financial Services research shows how informal and formal financial tools coexist in Nigeria, including savings behaviours like Ajo and Esusu. In rural areas where bank branches are scarce, the percentage is even higher. The system persists not because it is perfect, but because it serves a purpose that formal banking does not: community-based, flexible, and accessible saving without account minimums or paperwork.

The Trust Problem: When the Collector Runs Away

For all its strengths, traditional Ajo has a critical vulnerability. It relies entirely on trust in the collector. The collector is the person who holds everyone's money between collection day and payout day. They are the one who walks around with ₦100,000 or ₦500,000 in cash. And sometimes, that temptation proves too strong.

Stories of Ajo collectors disappearing with members' money are tragically common across Nigeria. A market woman in Ibadan collects contributions from 20 fellow traders for six months, building up nearly ₦1 million, then vanishes. A church Esusu group finds out their trusted treasurer has been using members' contributions to fund personal expenses, hoping to repay before payout day. The scheme collapses when the debt becomes too large. These stories are so frequent that many Nigerians have personal experience with a failed Ajo. Informal savings groups can create trust, record-keeping, and payout-coordination challenges, especially when members rely on manual tracking. That is money that families saved for school fees, medical expenses, and business capital, lost because there was no system of accountability.

The problem is structural. In traditional Ajo, there is no contract, no third-party oversight, no escrow, and no recourse. If the collector disappears, the group's only option is to track them down through social networks. Often, the collector has already left town. Even when they are found, getting the money back requires negotiation, family pressure, or sometimes police involvement, none of which guarantee recovery. This trust problem has always been the weak point of informal group savings. It is the reason many Nigerians who trust banks (despite their fees and bureaucracy) avoid traditional Ajo. And it is the problem that digital solutions are best positioned to solve.

How Digital Tools Are Modernizing Group Savings in Nigeria

The digital transformation of Nigerian fintech has not left group savings behind. Several platforms and approaches are bringing Ajo and Esusu into the app age, each solving different parts of the traditional system's problems.

Platforms Modernizing the Savings Side

- Cowrywise Savings Circles: Cowrywise introduced savings circles that mirror the Ajo structure. Members contribute funds that are pooled and paid out on a rotating basis. Cowrywise holds the funds instead of a human collector, which reduces the risk of theft or disappearance. The platform handles the math, timing, and disbursement.

- PiggyVest Group Savings: PiggyVest, Nigeria's most popular savings app, offers group savings features where friends and family can save toward a shared goal. The funds are locked in the app, and members can track progress together. While PiggyVest's group features are more focused on shared goals than rotating payouts, they represent the same underlying principle: digital trust replacing human trust.

- Traditional Cooperatives Going Digital: Many existing cooperative societies and thrift associations in Nigeria are adopting digital tools. Some use simple solutions like dedicated bank accounts with multiple signatories. Others use apps and USSD codes to track contributions and manage payouts. The shift from cash-in-hand to digital record-keeping is reducing errors, disputes, and fraud across thousands of cooperative groups nationwide.

The Missing Piece: Group Money Distribution

Digital savings platforms solve the collection and holding problem. They ensure contributions are safe, tracked, and accessible. But they do not fully solve the distribution problem. When it is time for a member to receive their payout, the money still needs to reach them. With traditional Ajo, the collector handed cash directly to the recipient. With digital Ajo platforms, the money can be transferred to the recipient's bank account. But this is where a new bottleneck emerges. Not everyone in a savings group uses the same bank. Not everyone has a traditional bank account. And transferring money to 10 or 20 different people, each with a different bank, a different account number, and a different preferred receiving method, is a logistical headache that many savings groups struggle with.

This is where the pass-through model changes the game. Instead of an organizer collecting money from everyone, depositing it in a central account, and then initiating individual transfers to each recipient (a process that takes hours and introduces multiple points of failure), a pass-through system lets the organizer set up a single payout pool. Recipients claim their share using just their phone number. Successful claims are processed through supported payment partners to the recipient's OPay, PalmPay, or Moniepoint account. No account numbers to collect. No multiple sender transfers to initiate. No Goodiebag wallet withdrawal step.

Goodiebag fits naturally into this gap. An Ajo organizer can fund a single Goodiebag with the total payout amount for the cycle. Members receive the link and PIN. Each person claims their share to their OPay, PalmPay, or Moniepoint account. The organizer handles one transaction instead of ten. Members get typically processed quickly without sharing their bank details with anyone. The group's payout process becomes as digital and frictionless as the collection process. For a savings circle of 20 people each receiving ₦25,000, the organizer saves roughly an hour of manual transfer work and eliminates the risk of sending money to the wrong account.

Create your first Goodiebag

Create a money packet in under 2 minutes. One link. One PIN. Everybody paid.

Create a GoodiebagHow a Digital Ajo Group Can Use Goodiebag for Payouts

A modern Ajo group can run a full cycle with digital tools for both collection and distribution.

- 1Collection phase: Members contribute their weekly or monthly dues to a digital savings platform (Cowrywise, PiggyVest, or a cooperative bank account). The platform tracks who has paid and who has not. No cash changes hands. No collector carries money through traffic.

- 2Payout calculation: At the end of the cycle, the organizer knows exactly how much each recipient is due. The total pool is verified against the digital records. Disputes are rare because every transaction is logged.

- 3Distribution via Goodiebag: The organizer visits getgoodiebag.com, creates a new Goodiebag with the total payout amount, sets the number of recipients to match the cycle participants, and selects Lucky Split (for system-determined variable amounts) or Equal Split (for identical payouts). They pay once using a Paystack-supported payment method, such as card, bank transfer, USSD, or any option shown at checkout.

- 4Share and claim: The organizer shares the Goodiebag link and PIN with group members via WhatsApp, Telegram, or SMS (depending on the group's communication channel). Each member opens the link, enters the PIN and their phone number, and successful claims are processed to their OPay, PalmPay, or Moniepoint account.

- 5Confirm and close: Members confirm receipt in the group chat. The organizer closes the cycle. Any unclaimed funds (if a member misses the 24-hour window) return to the organizer automatically.

Practical Tips for Starting a Digital Ajo Group

Read Also

If you are considering starting a digital Ajo or Esusu group, here are practical guidelines based on what works in Nigerian communities today.

- 1Start small: Begin with 5 to 10 trusted people. You can expand the group once the system is running smoothly and members are comfortable with the digital process.

- 2Use a digital collection tool: Choose a platform like Cowrywise or PiggyVest for collecting and tracking contributions. Avoid cash-only collection. The whole point is to eliminate the trust risk of a human holding money.

- 3Set clear terms in writing: Even in an informal group, write down the rules. Contribution amount, frequency, payout order (lottery or need-based), consequences for late payment, and the process for adding or removing members. Share this document with everyone.

- 4Use Goodiebag for payouts: When it is distribution time, use Goodiebag to handle the payout to members' OPay, PalmPay, or Moniepoint accounts. One payment from you. Typically fast receipt for everyone. No chasing people for account numbers.

- 5Keep a digital record: Maintain a simple spreadsheet or Google Sheet tracking who has paid, who has received, and when the next cycle starts. This prevents disputes and gives the group a clear history.

- 6Communicate in your group chat: Most Ajo groups already use WhatsApp or Telegram. Use the same channel for reminders, payout announcements, and celebration. The social energy of a group seeing payouts happen in real time is part of what makes Ajo work.

- 7Plan for emergencies: Agree upfront what happens if a member cannot make a contribution. Can they skip a cycle? Can someone lend them the amount? Having a policy before the emergency arises prevents resentment.

The Future of Group Savings in Nigeria

Group savings in Nigeria are changing, but Ajo is not disappearing. It is too woven into markets, churches, mosques, and rural communities. Digital tools simply solve some of the old pain points: cash handling, record keeping, reminders, and payout disputes.

The future likely looks like a hybrid. Collection will happen through digital savings platforms that offer transparency and security. Payouts will happen through transfer systems like Goodiebag that eliminate the distribution bottleneck. Communication and coordination will happen through WhatsApp and Telegram groups that maintain the social bonds that make group savings work in the first place. The community spirit of Ajo and Esusu will remain. The cash, the trust risk, and the logistical headaches will fade away.

We are already seeing early signs of this hybrid model. In Lagos, some market associations have moved their Ajo contributions to bank transfers while keeping their WhatsApp group for coordination and social bonding. In Enugu and Onitsha, savings circles are using Cowrywise for collection and Goodiebag for payouts, creating a fully digital cycle that retains the community feel. In Kano, Adashe groups are experimenting with mobile money solutions that bridge the gap between informal savings and formal financial systems.

For fintech platforms building for Africa, the lesson is clear. You cannot simply replace Ajo. You have to improve it while respecting what makes it work. The social trust, the community obligation, the shared goal. These are not bugs in the system. They are features. Digital tools should reinforce them, not erase them.

The Bottom Line on Ajo, Esusu, and Digital Group Savings

Ajo and Esusu are not relics of the past. They are living, evolving financial systems that have served Nigerian communities for generations. The core insight of group savings, that people achieve more together than alone, is as relevant today as it was a century ago. What has changed is the technology available to support it.

Digital tools solve the three biggest problems of traditional group savings: the risk of theft or disappearance by the collector, the lack of records and accountability, and the logistical burden of distributing money to multiple recipients. With the right combination of platforms, a modern Ajo group can enjoy all the social and financial benefits of the traditional system without the hazards. The collection is transparent. The funds are secure. The payouts are fast. And the community bonds are stronger, not weaker, because everyone can see the process working.

If you are part of a savings group or thinking of starting one, consider going digital. Use a trusted platform for collection. Use Goodiebag for distribution. Keep the WhatsApp group for the energy, the accountability, and the shared celebration when each member receives their payout. The tradition of Ajo and Esusu is too valuable to lose. It just needs better tools. And those tools are here now.

Goodiebag should only be used for social gifting, appreciation, and payout coordination where legally appropriate. It should not be used to collect deposits, manage savings schemes, operate investment pools, or run regulated financial services.

Goodiebag Editorial Team

Goodiebag product and safety team

Guides by the Goodiebag team on social cash gifting, supported payouts, sender safety, and practical digital reward use cases in Nigeria.

Start your first Goodiebag today

Fund a drop, share a link and PIN, and let your audience claim while the moment is live. No Goodiebag account needed for recipients.

Create a Goodiebag